A Movable Threshold for Municipal Pension Adjustment

The three components of Governor Chafee’s legislative package are notable distinguishable in one important respect: when they become available to municipalities.

The legislation granting the Department of Education “new powers” of local-budget oversight appears to apply across the board. As I’ve previously described, the section providing mandate and other relief for struggling municipalities is extremely restrictive in its application and applies ever-shifting criteria for determining which municipalities are eligible.

The one component of the package that appears to draw a reasonably available threshold is the “Critical Plan Empowerment Act,” which allows any pension fund that dips below a 60% funding ratio to suspend cost of living adjustments (COLAs). (That reform is in addition to reductions of disability pensions and caps on local pensions that would apply across the board, going forward.)

One problem with the threshold — ultimately making it movable, as well — is that various assumptions can change upon a vote of the Retirement Board. A change in the expected return on investment of the pension fund (i.e., the discount rate), for notable example, can swing the funding ratio dramatically. Indeed, the immediate crisis that last autumn’s pension reform was meant to forestall occurred when the Retirement Board adjusted assumptions, including a drop of the discount rate from 8.25% to 7.5%.

A commentary piece by Mike Stenhouse and Rich Danker for the Center for Freedom & Prosperity makes the point by referencing a working paper by Eileen Norcross and Benjamin VanMetre of the Mercatus Center prepared in the midst of the pension reform debate. Norcross and VanMetre make the point that pension funds should be estimated and funded in accordance with private-sector funding ratios.

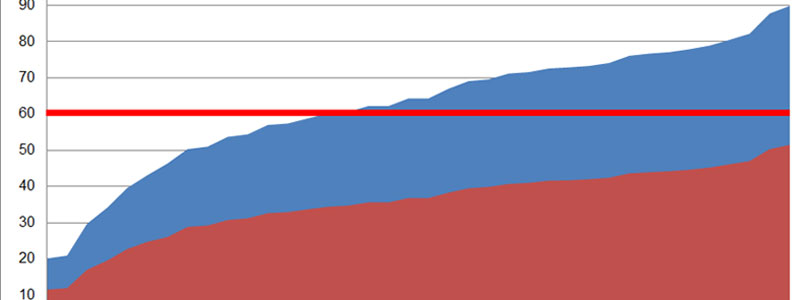

If we apply that principle to the governor’s new legislative package, the result looks like this:

On that chart, showing the funding ratios for all Rhode Island municipalities except Exeter in order of increasing funding level, the blue area represents the funding ratios at a 7.9% funding ratio. At that rate, not even half of municipalities would be eligible for Chafee’s COLA exemption, which is represented on the chart by the bright red line.

The blood-red area, by contrast, shows the funding ratios using the Mercatus Center’s recommended return-on-investment assumptions. Under that, more realistic, analysis, every city and town ought to be eligible.

Where thresholds and discount rates and every other assumption ought to be is certainly subject to reasoned debate. By the same token, however, it’s also susceptible for undue political adjustment.