Using Providence for Pension “Liability” Perspective

It turns out that I’ve been significantly wrong in my conceptualization of Rhode Island’s pension problem. Fortunately, it doesn’t affect anything that I’ve written thus far (which is why I didn’t discover the error until now), but it does clarify some of the mystique that surrounds actuarial calculations.

The problem centers around the use of the word liability.

A typical dictionary definition would offer “money owed.” If somebody says you’ve got a $200,000 liability on a home, it means you have to come up with that much money to cover the property. If you invest in a business and have, say, a $75 million liability should it fail, it means that collapse of the investment will cost you $75 million.

So, if an actuary tells you that your total liability for a pension plan is $1 billion in the context of an amortization period, that means that you’ll have to come up with $1 billion by the “date certain” at which point the plan will be fully funded, right? Wrong.

An actuarial report publicized during the state’s pension reform debate offers a reasonably clear definition of the actuarial usage of the word:

The actuarial accrued liability is equal to the present value of all benefits less the present value of future normal costs. The unfunded actuarial accrued liability (UAAL) is then determined as (i) the actuarial accrued liability, minus (ii) the actuarial value of assets.

Translating that into layman’s terms is where things get confusing. Basically, the paragraph defines the total “liability” as the amount of money that the plan would have to have in the bank right now in order to fund pensions forever. That’s in addition to the city or state’s annual payments. The “unfunded liability” is therefore the amount that the city or state would have to come up with right now on top of what it already has in order to get back on track.

For a little more detail: The actuaries come up with a “normal cost,” which is supposed to be the annual payment that will totally cover all pension benefits for an employee’s retirement if the payments are made every year for his or her entire career. In theory, that way, the city or state only ever pays for people who are currently working and is never paying somebody to do a job while still paying the people who used to do that job.

So, they figure out the total benefits that have been promised to all employees. Then, they “discount” that total by the amount of outside money they expect from investments; that’s the “present value.” Next, the actuaries add all of the future “normal cost” payments to all of the investment returns that those payments will earn at the discount rate. Subtracting the normal cost from the benefits tells them how much they would have to have in the bank right now for investment earnings to cover all of the benefits that have been promised. The amount that they don’t have is the unfunded liability.

When we hear, therefore, that Providence has a $901 million unfunded pension liability, that doesn’t mean that it has to come up with $901 million in the next 28 years (which is the amortization period), as a layman’s understanding of “liability” might suggest. Rather, it means that Providence needs that much money immediately. If the city made no payments beyond its normal costs, the unfunded liability would grow every year.

The distinction became clear, to me, while looking at this chart from Ted Nesi. It shows the assets staying the same no matter the discount rate, and it shows total liability as the assets plus the unfunded liability. The way I’d been thinking about the problem (and the way I think most non-finance people would), the “total liability” ought to stay the same, with the amount the city actually has to pay into the system changing depending on its investment returns.

The obvious next question is what Providence is really liable for. Since a pension plan is a continuous program, not a limited-time expense, there are multiple ways to answer. (Please see the very important note at the end of this post.)

First, we could look at the total amount that Providence expects to pay out to retirees over the amortization period. The latest reports that the city provided to the state give annual dollar amounts for a “pay as you go” system, which should suffice as a stand-in for payouts.

Summing all of the “pay as you go” numbers for the amortization period (through 2040) gives a total “liability” of $3.8 billion. The problem is that such an approach means the annual payments never really drop, because the city will always be paying for retirees at the same time that it’s paying for current employees, essentially doubling the payroll or more. In other words, the amortization period is arbitrary, because the real liability is infinite as long as the pension system is still being promised to new employees.

Using the actuaries’ definition of “actuarial accrued liability” (i.e., what is needed now beyond what will be paid later), the documents show the total as $1.3 billion with a discount rate of 8.25% (an investment assumption well above all but one of the other pension systems in Rhode Island). So, another way to look at the total amount of money for which the city is liable would be to run the numbers again using a discount rate at 0%.

In theory, that would tell us the total amount that must be put into the Providence pension system — that the people of Providence are ultimately responsible for adding to the system, one way or another — by the end of the amortization period in order to continue normally from there. Unfortunately, none of my calls to Providence’s actuaries, Buck Consultants, have been returned, so I’ll have to improvise from what’s publicly available.

For this total, we add the total assets at the end of 2012 to all of the annual payments that the actuaries require up to 2040, add in all of the benefit payments listed under “pay as you go,” and then factor in all of the expected returns at 8.25%. (That’s necessary to figure out what the actuaries think the pension system has to have earned or paid out by 2040.) Note that I assumed payments and payouts are evenly spaced throughout the year, so the system theoretically earns returns on half of its contributions within the year that they’re made.

One way or another, the City of Providence has to make sure that $5.7 billion has been added to the pension system or paid out to retirees between now and 2041. In a conversational understanding of liability, that is where the city stands. (Again, see the very important note below.)

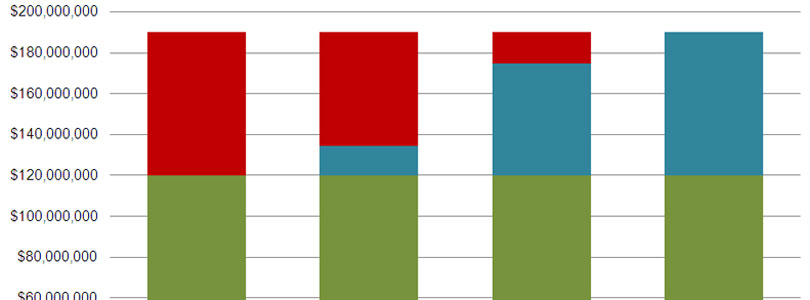

Such a long-term definition of liability isn’t but so useful. It would be more useful to bring the debate back to annual dollar amounts. For the following chart, I divided all of the predicted payments, payouts, and investment returns by 28 years. That annualized liability — what the city has to produce for the pension system in an average year above the assets that it already has — comes to $189.9 million, or roughly 30% of the budget that Mayor Angel Taveras just proposed.

For a proper perspective, I’ve presented the total with several possible rates of return: the current 8.25%, the state’s 7.5%, and the 4% fixed-income return that some experts argue ought to be the discount rate. The green block is the average dollar amount that the actuaries are already calling for the city to make. The blue block is the expected return. And the red block is the additional money that would have to be procured if the return comes in at the percentage shown.

One area of additional confusion that readers ought to keep in mind is inflation. The discount rates (or investment returns) build inflation into them. In general, three factors go into the discount rate: increased value of the asset, increased investment value of the asset, and inflation. A discount rate of 8.25% means that every $100 of assets will be worth $108.25 next year because (1) the assets will be worth more (think of owning a percentage of an expanding company), (2) the assets will trade at an even higher rate on the market, and (3) the economy overall will inflate.

The actuaries’ list of all future payments adjusts for inflation, so the $185.0 million payment called for in 2039 will actually be worth about the same as 2013’s $72.1 million payment, if the inflation assumption holds. In real dollars, then, the average “current payment” shown in the chart would be much easier to pay at the end of the amortization period than at the beginning. I should stress, though, that this is an exercise in perspective, not in exact dollars.

Inflation caveats aside, the above chart gives a sense of how a high discount rate allows politicians to keep down the amount of money that must be put aside each year to fund pensions. A more rational (more conservative) method of budgeting for pensions would compare a previous year’s actual investment return to what it was supposed to be and require the city or state to add some actuarially determined sum to the next year’s payment. In the absence of such prudent measures (or incredible luck), the liability is only going to grow, no matter the definition.

Not only is every dollar not realized in investments this year added to the liability, but so is every cent in investment returns that dollar will never make.

A Very Important Note

The liabilities described in this post are all low, possibly for two reasons. First, employee contributions do not appear to be differentiated. If employee contributions are separate from those shown, then the discount rate would affect them, too, the city would ultimately be liable for making up the difference if investments fall short.

Second, and more certain, is that the dollar amount required in 2040 assumes an 8.25% return thereafter. If investment returns are expected to be lower than that, then more would have to be in the bank on that date in order for the plan to be 100% funded.

Another Note

Ted Nesi writes to correct one of my assumptions: Apparently, Providence makes its annual payment the October after the end of the fiscal year, not spaced throughout. I haven’t changed the above calculations, though, because I folded the annual 1/2 credit with a 1/2 deduction for payouts when figuring out the amount of actual interest expected, meaning that it isn’t quite so easy to make the adjustment. It would likely change the total liability less than $100 million, so in the big picture, it wouldn’t be a significant change, especially for a conceptual calculation.

It’s good to know, though!